Why not Pensions, the Stock Market or Precious Metals or even a regular Savings Account?

Different investments come with different levels of risk and different levels of reward. You need to decide what is right for your current situation and what aligns with your future goals. Here i will give an outline of the performance of some investment options, and go into more detail about the benefits of investing in property. If you are uncertain about what is right for you, then you should seek the advice of a qualified financial advisor.

How does Property Compare?

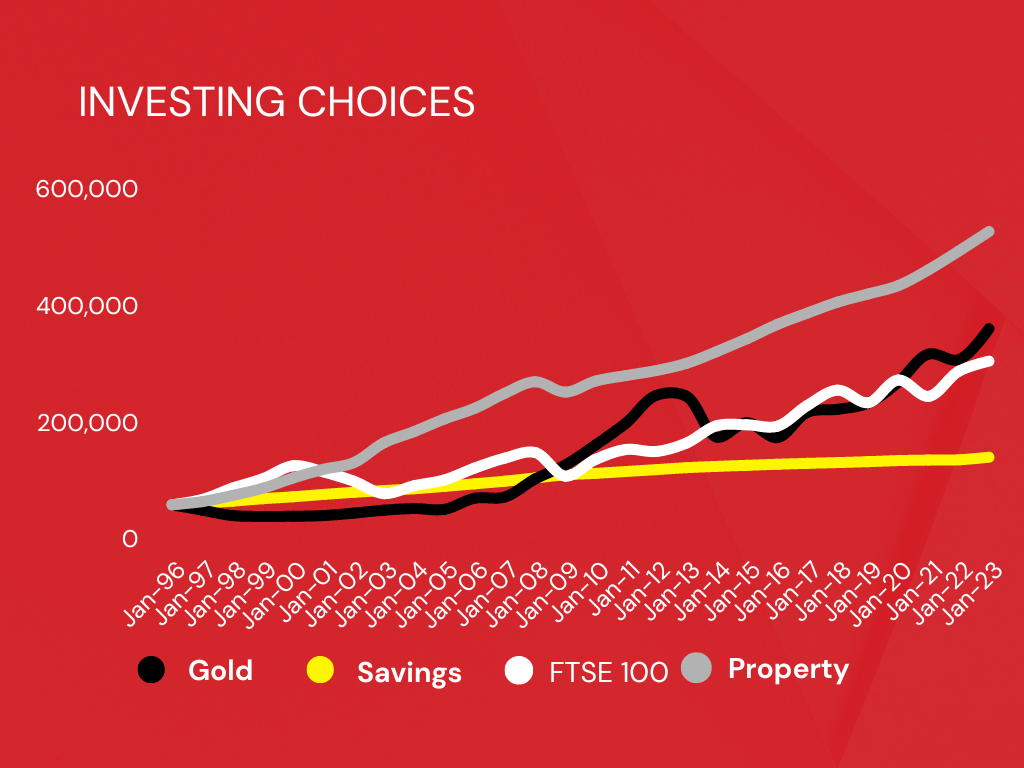

Imagine you had £60,000 to invest in 1996. What would have been your best choice?

The easiest option is probably just put the money into a savings account and leave it to compound over the years. This is very low risk, and by now it would be over £140,000.

Investing in gold, also very low risk, would have given about £360,000; and investing into an ETF that tracks the FTSE 100 would have produced about £300,000 if you kept re-investing the dividends each year. Although Gold and Stocks clearly have more reward than a savings account the main downside is that if you need to take the money out for any reason you may have to do so at a time when the price or value is depressed.

In 1996, £60,000 was enough to buy an average house and pay any purchasing costs. If you had paid the rent into a savings account and left it to compound, then the value of the house and the rent are now over £500,000.

Risk versus Reward

Buying a property does come with extra work – finding the property, completing the purchase, and finding and managing tenants. In addition there is extra risk – mainly in the form of tenants not paying the rent, or of potential problems with the property. Houses are also less liquid than the other options, and similar to investing in Stocks or Gold if you need to sell you may have to do so at at time when prices are lower. When choosing where to keep your money you need to weigh up these risks and decide if the extra rewards make those risks worth taking for you.

Property's Biggest Advantage

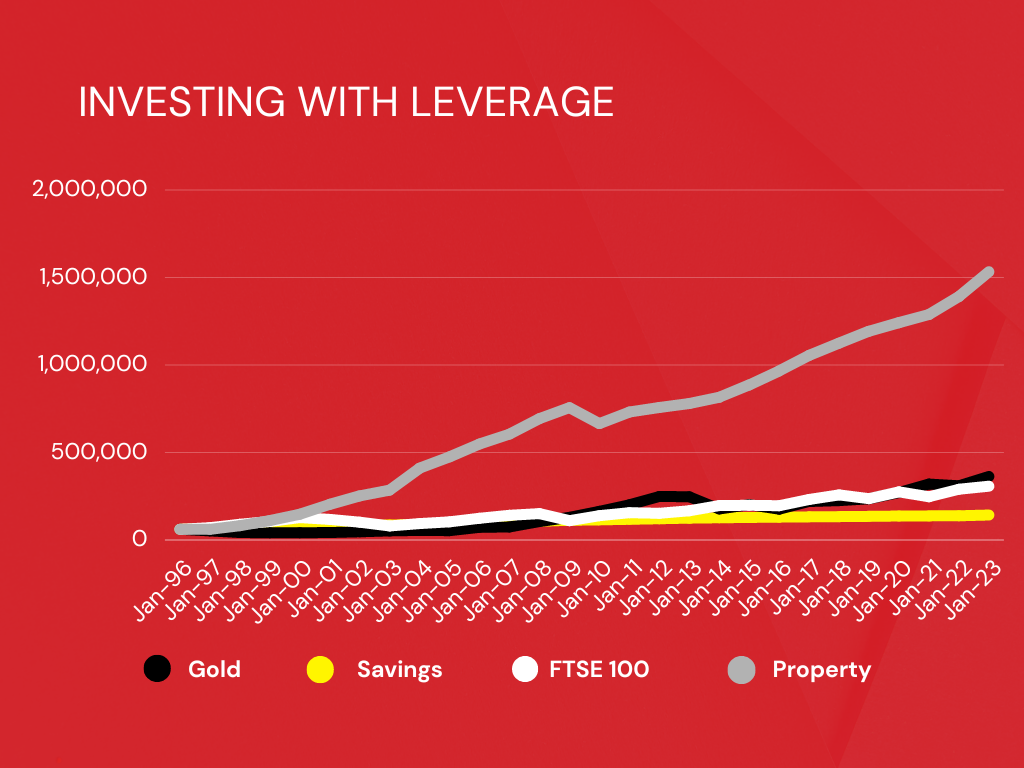

Investing with Leverage

Since 1996 it has become possible to buy property using a Buy To Let Mortgage. This gives the property investor leverage in a way that cannot be done with Savings Accounts, Gold or Stocks and Shares. Essentially with a Buy to Let mortgage the investor typically puts down 25% of the value of the property; pays an interest only mortgage on the remaining 75%; and rents the property out for more than the cost of that mortgage.

Does a mortgage add more risk?

If instead of buying 1 house for £60,000 in 1996 you bought 4 houses splitting your money into 4 deposits of 25% in each property while taking out buy to let interest only mortgages; then the returns would have been significantly higher.

Solely in terms of the equity now built up in the portfolio of properties you would be close to £1 million. If you had also paid all your rental profit into a savings account allowing it to compound, in total including the equity you would have over £1.5 million. Yes ….. £1.5 million.

You could also have remortgaged the portfolio at least once in that time and used some of the accumulated rental profit to buy further rental properties which would have accelerated the growth further still.

It may be perceived that the mortgages are additional risk as you have to pay these even if your tenants do not pay you. However, with 4 properties you now have 4 tenants, so if 1 tenant stops paying you still have 3 tenants and their payments will cover the one missing payment until you get a new tenant in place.

The longer you invest the higher the returns. The sooner you start the longer you will be invested.